Last week we examined the startup of deregulation, why a competitive market for electricity is difficult and early failures. This week, we look at the price impacts and some long-term implications of deregulation.

It seemed to me that deregulation of the electricity market had been a disaster: bankruptcies, soaring prices, and most recently, stranded baseload assets. There was a lot of evidence in that, but lately, prices have improved, but other challenges are emerging.

Deregulation’s Impact on Pricing

I realized that searching for comprehensive data showing the impact on electricity costs for regulated versus deregulated is impossible. Lucky for you, I mined data from several sources and pulled it all together[1].

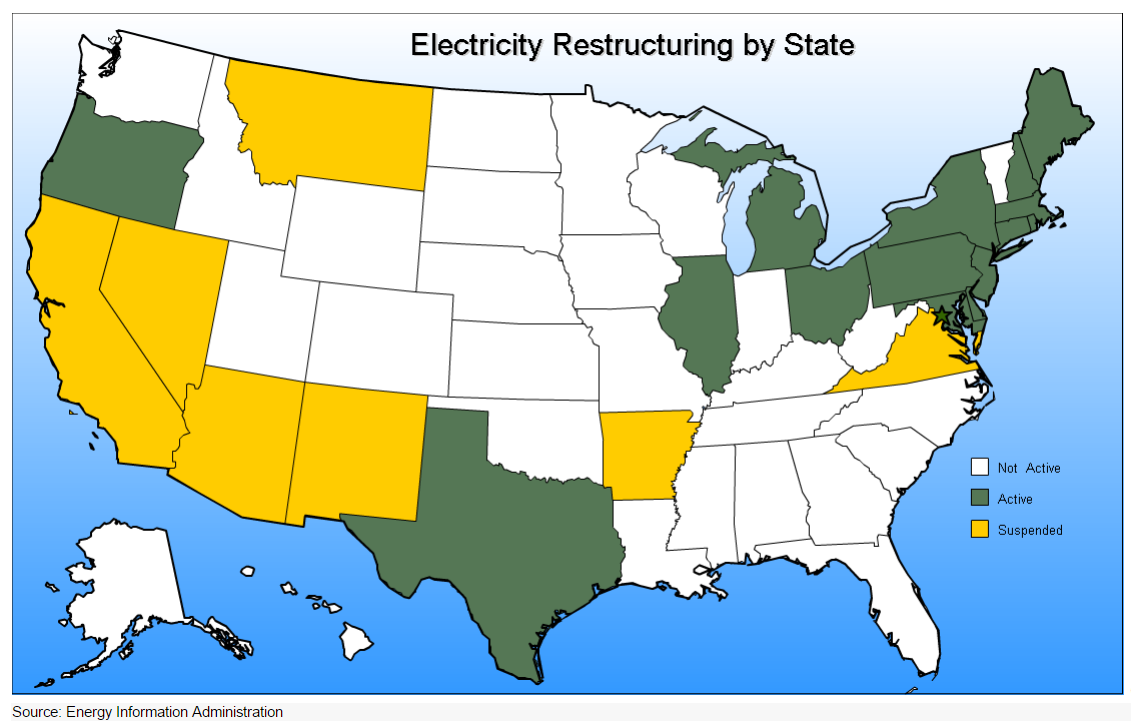

My analysis is based on the DOE-sponsored map below and gruesome data sets provided by the Energy Information Administration.

Full disclosure: per my read of things, Michigan only deregulates 10% of its sales, so I count Michigan in the regulated column.

Deregulation hit full speed in most states at the time of the California crash described last week; around 1999-2000. Therefore, I looked at data from 1998 through 2014. While doing my research, I found articles posted in the middle of this period describing the failures of deregulation, and then later how deregulation was finally starting to work. As a result, I took snapshots at 2007 and 2010 to see what happened along the way.

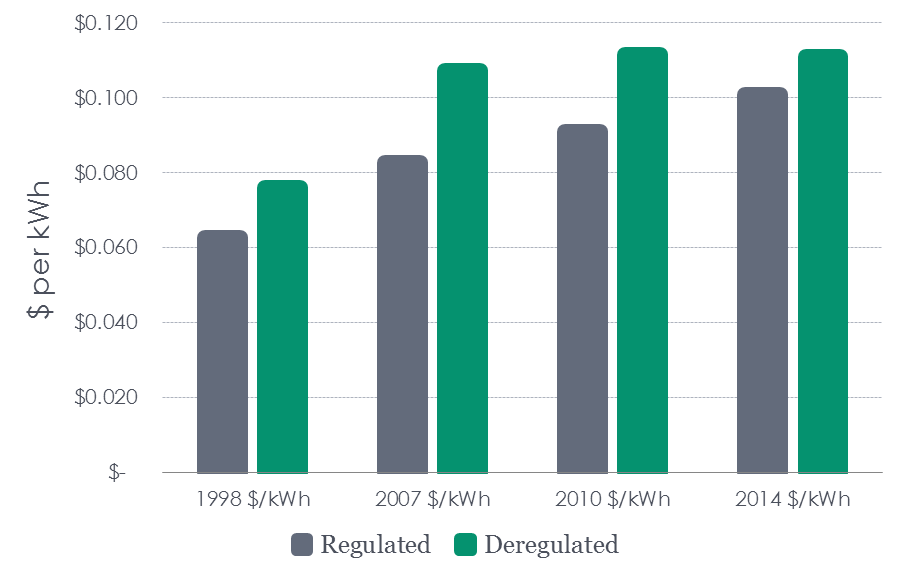

The first chart to the right shows the cost per retail kWh, weighted in deregulated states versus regulated states. The second chart after that shows the percent change in retail price by year with a baseline of 1998 prices.

Finding #1: Electricity costs more in deregulated states compared to regulated states, just as I thought.

Finding #2: Reports are correct that prices in deregulated states shot up fast in the early years.

Finding #3: Prices in deregulated states have leveled off.

Finding #4: Prices in regulated states have increased linearly and outpaced price increases in deregulated states.

What’s Going On?

In 2010, Forbes reported that “Electric Deregulation Finally Takes Off”. Forbes says that after years of (deregulated) price increases, prices are finally falling because technology that was formerly only available to big industrial customers is trickling down to smaller users. They credit the smart meter and real-time pricing, essentially.

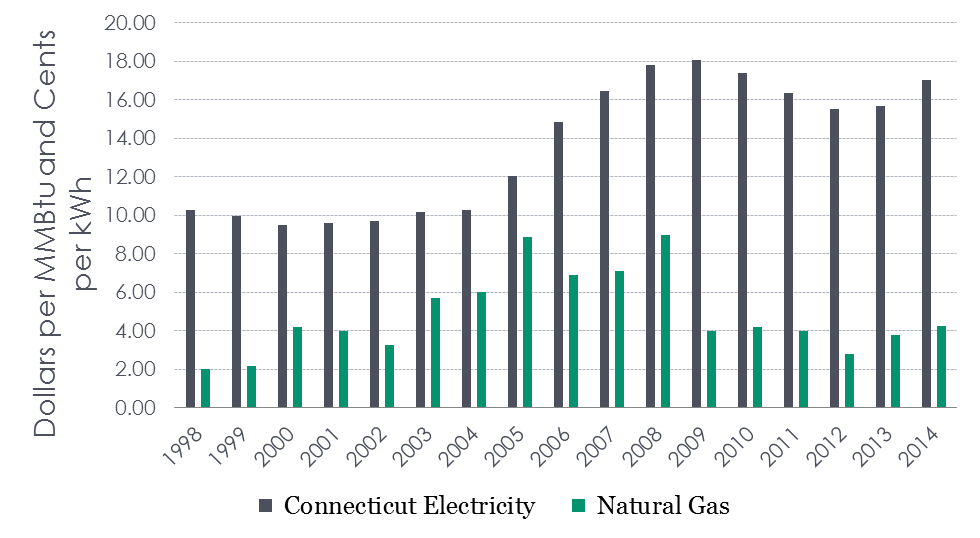

Smart meter technology makes for quaint theory. In reality, two other major factors are at play: hydraulic fracturing or “fracking” for natural gas and wind energy. They are responsible for the miraculous electricity price containment. This is demonstrated in the next chart showing average retail electric prices for Connecticut versus average annual natural gas prices[2]. The correlation seems pretty clear. The impact of wind is reported to the left.

Trouble Brewing

Deregulated utilities did well under deregulation for the first ten years. Then fracking happened, and now resource constraints in the east are making stakeholders nervous.

I wrote about deregulation risk recently in Betting With Deregulation – A Risky Proposition. You can read the details, but it includes a few examples of changing one set of rules (full regulation) to another set of rules (price floors). FirstEnergy and AEP (Ohio) liked deregulation when they held the cheap generating assets, but now they are stuck with these albatrosses and uh, want a bailout. The PUCO said yes. The FERC said NO!

The FERC is right. Uncertainty planted by changing the rules every few years keeps would-be market entrants on the sidelines, and that will not end well for rate payers in future years.

Latest Finagled Deregulated Regulation

As a result of the FERC smackdown on price supports for FirstEnergy’s and AEP’s money-losing coal plants, each is pursuing additional regulation. AEP decided to shut down its money-losing plants and is promoting reregulation. This is less shifty than FirstEnergy’s pursuit of a “grid modernization” rider, which will provide $204 million more revenue. It’s an end-around the FERC ruling to subsidize the “unregulated” money-losers with their regulated money maker (poles and wires). It’s already been approved by PUCO.

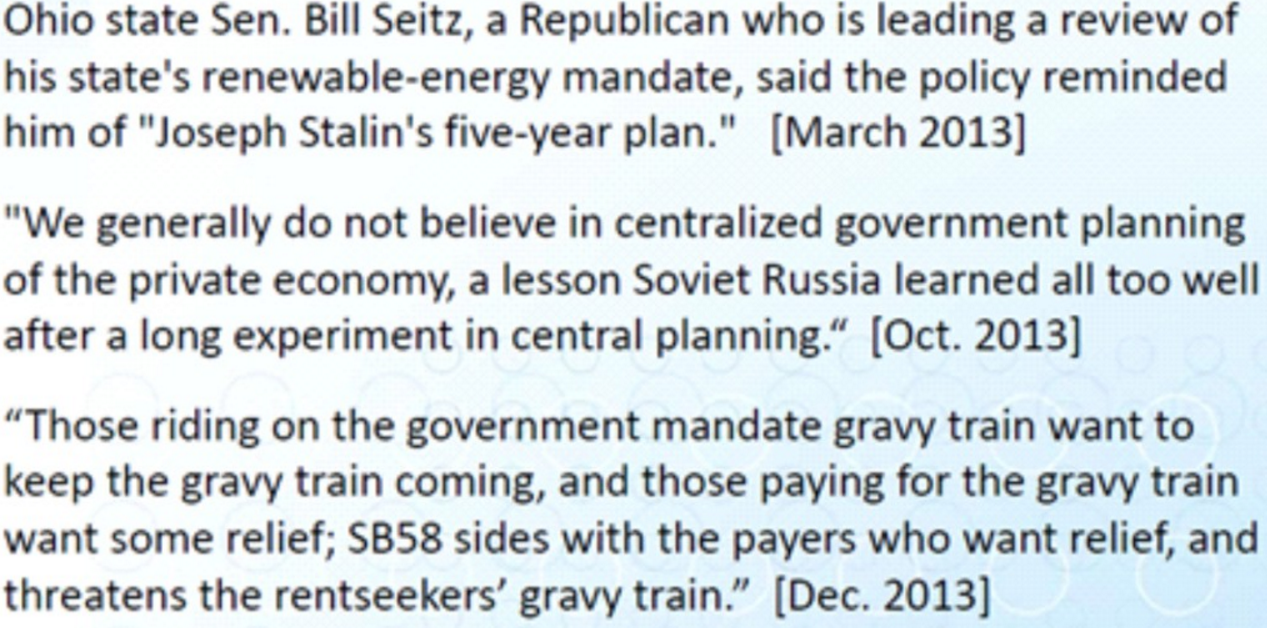

Just for fun, let’s go back a couple years to my post, “Energy Efficiency Under Attack – Stalin Would be Proud?”. That post quotes Ohio senators lambasting the waste of money and rip-off to customers that are energy efficiency and renewable energy standards.

It reminds me of an Austin Powers clip, “It seems the tables have turned again, Mr. Seitz.” I don’t think the money spent on efficiency, which benefited customers, was nearly $204 million.

The Problem for Baseload Plants

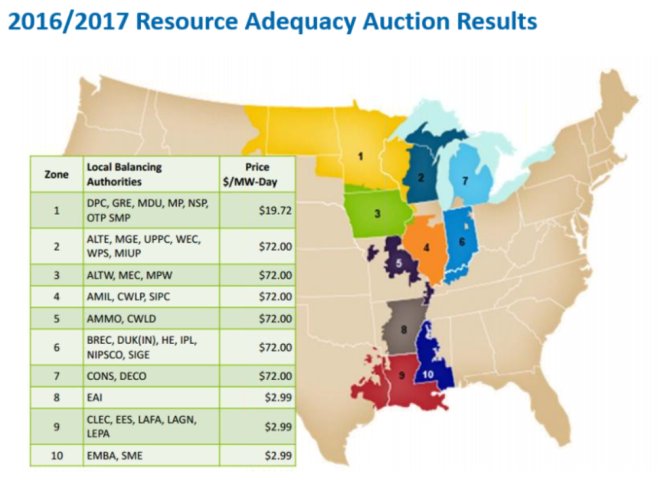

Refer to the Midcontinent Independent System Operator (MISO) chart below, courtesy of ICF. See the hole in the middle over Chicago. That is ComEd’s territory. They are part of PJM ISO, which includes Ohio, half of Kentucky, straight east to New Jersey, Pennsylvania, Maryland, and Virginia. PJM covers major shale gas territory, but it also connects many gigawatts of Midwest wind energy to PJM. You can see this in the pricing of the MISO load balancing authorities. The ones that border PJM have higher prices.

Natural gas and heavily subsidized wind drive down prices, most of the time. The problem is baseload nukes and coal plants need to run all the time to be profitable. They are only needed part of the time now with fluctuating wind and insufficient natural gas generation. We are seeing another subsidy of wind power coming – it’s the riders to keep these former baseloads online to fill the gaps left by wind power.

[1] Data table can be found here. It shows price changes and prices since 1998, by state. The first two are alphabetical by state, and the last one is sorted by 2014 prices, high to low. The purple states are the deregulated ones.

[2] Approximate from my read of the EIA natural gas price graph.

Join the discussion 3 Comments