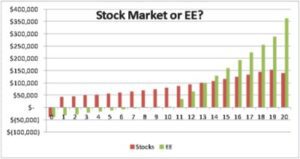

Last week we looked at the financial benefits of energy efficiency as compared to the stock market. I’m going to take this a few steps further, as forewarned last week. In both cases we start with the $39,000 investment and the stock market simply grows at its long-term average of 7.5% (Dow Jones Industrials). Obviously, a smooth appreciation of your investment is not the case and if you don’t have a strong stomach, you should avoid equities. Why is it called the Dow Jones Industrial Average anyway? It’s full of service companies, banks, and retailers. It includes Microsoft, but not Apple, which has over twice the market capitalization. A company like Apple, which is absolutely huge, would probably make up half the movement in the DJIA. The EE investment on the other hand immediately starts paying dividends – actually net cash in the bank to the tune of $6,200. This dividend shrinks as the interest payments, which are tax-deductible, go away until the lease/loan is entirely paid off. Over this period, the stocks, on average, would catch up to be almost exactly the same after 10 years. However, in the 10th year, the $30,800 annualized payments for the EE investment disappear and suddenly the investment starts earning 115% of the initial investment, year after year, for the next 10 years.

Stock Market or EE?

You may notice the dip at the end of the stock market valuation in year 20. That is the capital gains tax whack of 15% you have to pay when you cash out, wiping out the last few years of gains. There is no capital gains whack on the EE investment. All tax implications have run their course as they affect the annual energy savings, interest payments, and depreciation. Actually, in year 20 when the EE investment reaches the end of its useful life, the remaining value of the investment is fully depreciated. Since the depreciation period is 39 years, like that of any facility, almost 50% of the depreciation occurs at the end of life, resulting in a $44,000 surge in after tax income which is almost equal to one year’s energy savings.

Aside from generating over 250% the wealth generated in a stock market investment over a 20 year period, EE offers the very attractive benefits of risk mitigation and certainty for return on investment.

Energy prices are volatile and today there is as much uncertainty in energy prices as there has ever been, which is why investors and companies are sitting on the sidelines hoarding cash. Specifically, nobody knows how many power plants the EPA will eventually shut down. Will they allow hydraulic fracturing that has produced the glut and current rock bottom prices for natural gas to continue? The beauty of investing in energy efficiency is if prices go up, you save even more than you projected. Rising prices is not a good thing, but by investing in energy efficiency you have insulated yourself against this and even improved your ROI. Conversely, if energy prices fall, your ROI drops, but who cares? You are paying less and your profit, or after tax income, improves.

In IPO Return, Treasury Risk, I described the low risk in energy efficiency, in most cases. Whoever determines the savings potential must not be a dufus, hack, or cheat.

Everyone knows there is always competition for scarce capital within an organization. Very few investments (uses of capital) have the certainty of EE. If a manufacturer decides to add another line of production, they better hope demand for the product increases as projected. And by the way, what is the return on that product? 10%? What ROI does a grocery store facelift have? Is that going to result in $363,000 capital formation over the next 20 years?

How about risk in plain old strategy against competitors or to sedate rabid mobs of protestors? In this article, Holman Jenkins compares and contrasts McDonald’s response to heat from child obesity activism to that of Pepsi, which of course makes soda with the poisonous high fructose corn syrup and other salt/fat bomb stuff people, including me, love. Nacho cheese Doritos – mmmm! They were awesome in 7th grade and they are awesome in 2012. McDonald’s strategy was to add healthy stuff to their menu. Never mind, because nobody buys happy meals with apple slices. It makes them feel better just knowing healthy stuff is available (not making this up). Pepsi, on the other hand, apparently messed with its product line with poor results, no stock market gain in 5 years. The bottom line is business is fraught with risk at every turn. It’s very difficult to beat the low risk and high return of energy efficiency.

The only “downside” with energy efficiency is its potential for a given end user is capped. It’s like short selling a stock. The most you can make is the entire value of the sale. The most energy you can save is the total you are paying now. However, energy efficiency is far safer than shorting a stock. The downside of shorting a stock is infinite. There is minimal downside risk to energy efficiency.

Finally, to look at a couple factors, it is interesting that end of life value varies linearly with down payment and with corporate tax rate. The percent down makes little difference. Lower taxes are clearly a boon to energy efficiency.

Next week: I’ll be sure to find something to gripe about.