In the Energy Rant, I cover subjects I know well, subjects I don’t know well but can analyze with bookends and say, “that will never fly”, and things I don’t know well. It takes viscera, and that’s what I’m covering this week – not bowels, but utility rates impacted by energy efficiency.

Utilities are in business to make money, like every other business[1]. Let’s establish that making money or being profitable means revenue exceeds costs. Costs consist of long-term capital-intensive investments in poles, wires, and power plants; and operating costs including pesky employees, coal, natural gas, uranium, U.S. mail, trucks, ladders, and stuff like this.

All the operating costs are passed through to customers. Fuel prices go up – customers pay more, maybe not immediately, but eventually. However, although utilities pass operating costs like employees along to customers, they have incentive to reduce head count and keep rates low because keeping rates low makes it easier to raise rates when desired for investors. In one example, over the last ~15 years, one utility with which I am familiar shrunk their account management team (humans) from almost 50 to barely a dozen. Twenty years ago, customers, particularly old folk in bib overalls, would pay their bills to Esther at the local branch office. Esther is now gone, and the branch office is closed. Unless they are neighbors, 99% of customers know no one who works at a utility.

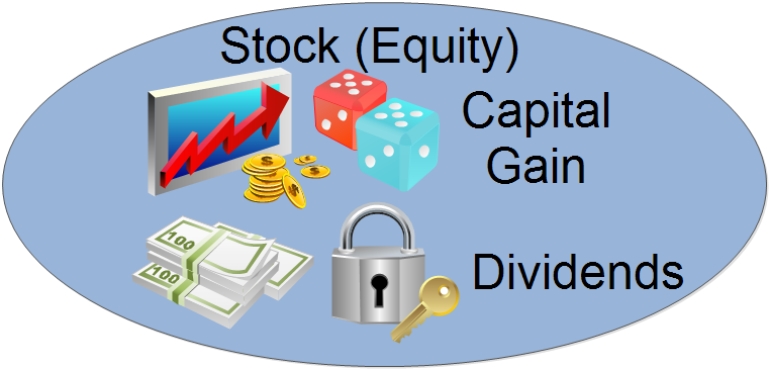

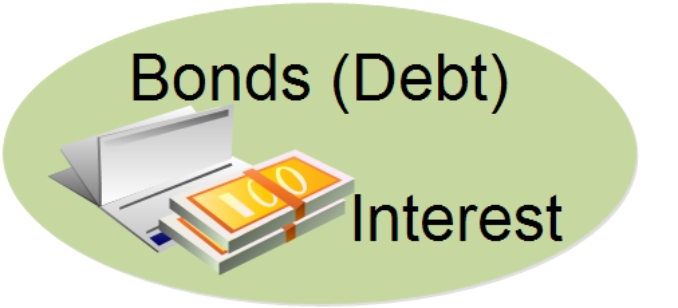

That capital intensive stuff is known as rate base, and it is the rate base on which regulators allow utilities to earn return on investment. Rate base is financed by debt (bonds or maybe bank debt) and equity (shares of stock). Interest paid on debt is a pass-through cost. Profit on equity is built into rates allowed by regulators – enough to make investment by shareholders worthwhile.

Quiz: why do shareholders invest in utility stocks? Why invest in any equities? One reason, which can be split into two reasons. The one reason is: you guessed it – make money. Making money is split into two: capital gain (buy low, sell high) and dividends (cash payments to shareholders). Or, investors can purchase debt in a utility in the form of bonds.

There is a range of risk in classes of stocks from startup tech or possibly biotech stocks at the risky end and low-risk stocks, or as my personal finance instructor called them, stalwarts, such as Coca-Cola. At the very low-risk end sits utilities. Good grief – think about it. Their customers are trapped. It’s a regulated monopoly. Bonds/debt in one way is less risky than stocks. If a company files for bankruptcy, bondholders are first in line to get their money out, unless the bonds were issued by a large auto manufacturer, in which case the federal government seizes control of the situation and embosses tire treads over the bondholders’ heads ignoring the rules of orderly bankruptcy reorganization.

Utilities make a stalwart company appear to grow at Mach 2.5 speed. For all practical purposes, there is no growth. Only fools would invest in utilities to buy low and sell high except for one factor, and I’ll get to that. Investors buy utility stock for stability and the dividend. It’s a diversified way to earn money, like an interest paying account or bonds. What I don’t understand is why the utility stock prices aren’t more sensitive to interest rates. In many ways, a utility stock is like a bond, paying a steady dividend. If I were a risk averse investor, I wouldn’t be whining about no return on fixed income securities (bank accounts, certificates of deposit, bonds, money market funds). Rather, I would be piling into utility stocks.

Is there energy efficiency in here anywhere? Yes. In exchange for a captive market, utilities relinquish price control to a third party – regulators. They also relinquish to some degree prospective growth as they cannot compete for current customers outside their service area. Enter energy efficiency. Energy efficiency either slows or reverses growth / rate base. If the rate base shrinks and the allowed earnings are a fixed percentage of rate base, shareholders get hosed because there is less dividend to be split among a fixed number of outstanding shares. What happens is, like bonds (should), the stock price inches down to maintain the yield (dividend divided by stock price). The prospect of further rate base shrinkage and dividend dilution can further drive down stock prices.

Here is a solution to treat shareholders well in a shrinking business (I haven’t seen this anywhere, unless it is cloaked in some other term): allow the utilities to earn enough to accumulate cash while maintaining a decent dividend. Use the accumulated cash to buy back shares. The share buyback provides stock price support and maintains yield for investors owning a shrinking rate base and dividend pay out. The dividend yield remains flat. I suppose this is decoupling, but it is a step beyond – an organized way to shrink a monopoly, and it is also a way to essentially treat energy efficiency as a resource – like rate base.

[1] Not in business as a public service to employ people, like the political class and many in the public seem to think.

Join the discussion 3 Comments